Protean eGov Technologies - Plumber behind India's digital identity, taxation and pension systems

AI + ME

Section 1. What the company does

The plain-English version

Protean is the quiet plumber behind India’s digital identity, taxation, and pension systems. When a citizen applies for a PAN card, Protean processes the application, prints the card, and delivers it. When someone opens an NPS pension account, Protean keeps a record of how much they contribute, where it sits, and what it is worth. When a bank needs to verify a customer’s Aadhaar, the API call often runs through Protean’s servers. The company does not own a brand that consumers know. Consumers see the IT department, PFRDA, or UIDAI. Behind those names, the systems that actually run the country’s identity infrastructure have been built and operated by Protean for three decades.

Founding story and the NSDL eGov rebrand

Protean was incorporated in December 1995 as NSDL e-Governance Infrastructure Ltd, a subsidiary of National Securities Depository Limited (NSDL), which itself was created to dematerialize Indian equity certificates. In 2003, the Income Tax Department awarded NSDL eGov the mandate to process PAN card applications. This was the founding moment of today’s Protean. By the late 2000s, the Pension Fund Regulatory and Development Authority (PFRDA) was created, and NSDL eGov became the first and dominant Central Recordkeeping Agency (CRA) for the National Pension System (NPS). The Aadhaar and eKYC layers came after. In December 2022, the company was spun off from the NSDL group, renamed Protean, and listed on the BSE and NSE in November 2023, with a market cap that briefly exceeded INR 5,000 crore.

The rebrand was not cosmetic. It signaled that the company wanted to be seen as a digital public infrastructure (DPI) builder, not just an NSDL appendage. The new identity opened doors to international mandates (Morocco, Ethiopia), private sector products (eSignPro, RISE API marketplace), and complex turnkey government RFPs (Bima Sugam, CERSAI CKYCRR 2.0, Aadhaar Seva Kendra). Three decades of running population-scale systems with 99.9% uptime turns out to be a hard thing to replicate. That is the moat.

Core value proposition: who pays and why

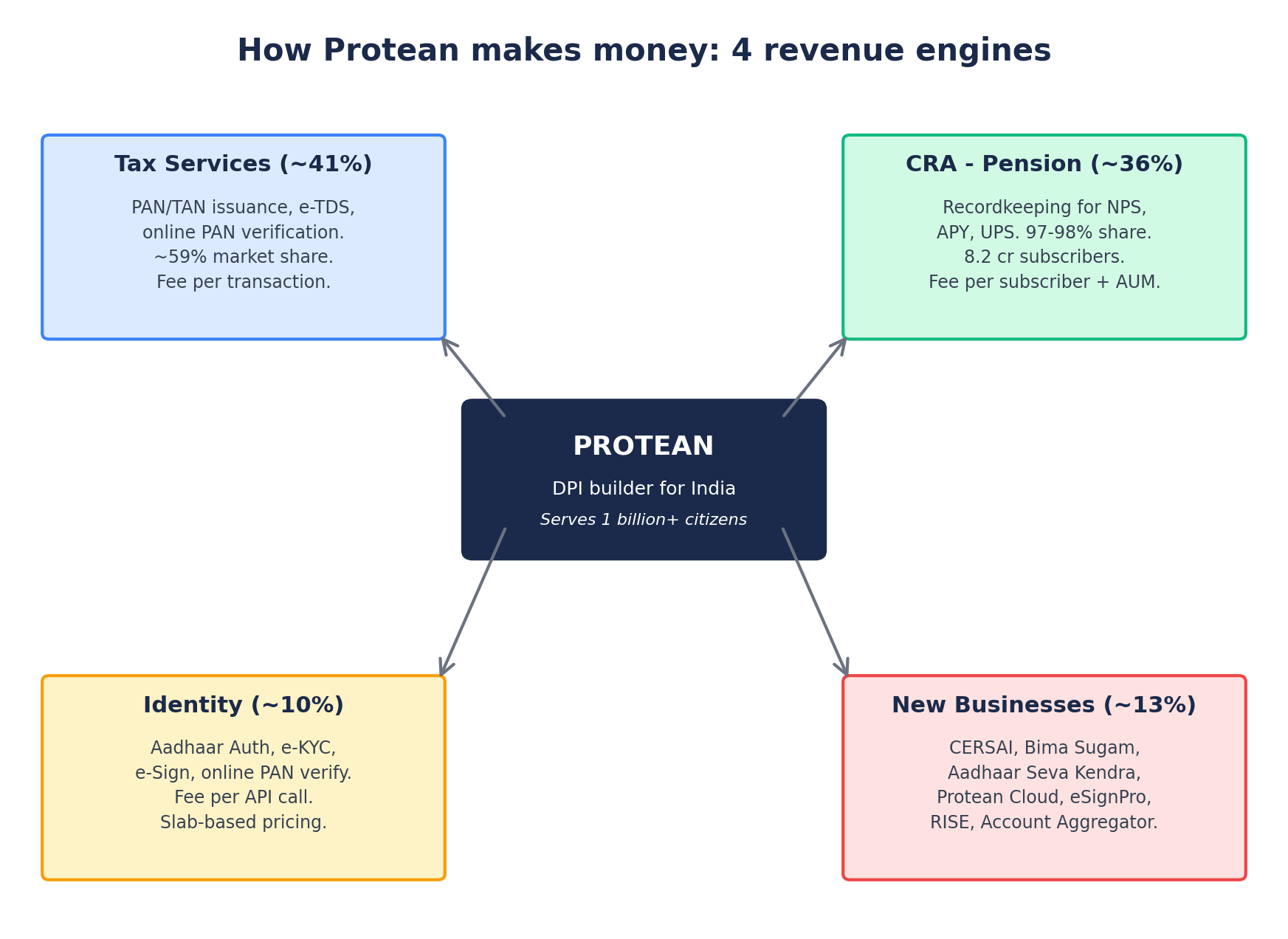

Protean is paid by three customer types. Government departments (Income Tax Department, UIDAI, PFRDA, CERSAI, IRDAI) pay Protean a per-transaction fee, or a fixed annual managed services fee, to run mission-critical systems. Banks, NBFCs, and insurers pay per API call when they verify a customer’s identity via Aadhaar, perform eKYC, or obtain an electronic signature. Citizens pay a service fee when they apply for a PAN card or open a pension account, paid directly or via an agent. Each transaction is small. The model works because Protean does very large numbers: 1.1 crore PAN cards in a single quarter, 35 lakh new pension subscribers per quarter, 8.2 crore cumulative pension subscribers.

How it actually works: a walk-through of one PAN card

Consider a citizen applying for a PAN card through a Protean agent in a small town. The agent (one of 4 lakh-plus assisted touchpoints that Protean operates across India) takes the citizen’s KYC documents, captures them digitally, and uploads them via a secure channel to the Income Tax Department’s PAN allocation system. The IT department’s tech stack performs deduplication and number issuance, returns the allotted PAN number to Protean, and Protean then prints the physical card and posts it to the citizen. Protean earns a fee for data collection, digital transmission, printing, and dispatch. The IT department keeps the data integrity work in-house (this is what PAN 2.0 is about). About 70-75% of all PAN applications in India still go through an assisted agent like this. The remaining 25-30% go online. Protean is paid in either route, though the fee economics are a bit different.

Why is this hard to replicate?

Three things take years to build:

Regulatory licenses (CRA, eSign authentication, KYC authorization)

Infrastructure trust (running a system with 8.2 crore subscribers requires audited operational discipline that takes a decade to demonstrate)

Distribution depth (the 4 lakh agent network was built over twenty years and is the reason citizens in Tier 3 and Tier 4 towns can access PAN, pension, and Aadhaar services)

A well-funded new entrant cannot conjure these overnight. This is the textbook definition of a regulatory and operational moat, even if the unit economics on any single transaction look fairly thin.

“We are very proud to share that Protean remains at the forefront of India’s digital transformation, need for driving inclusion or innovating and creating impact at scale.”

- Suresh Sethi, MD and CEO, Q2 FY26 concall, Nov 7, 2025

Section 2. Business segments deep dive

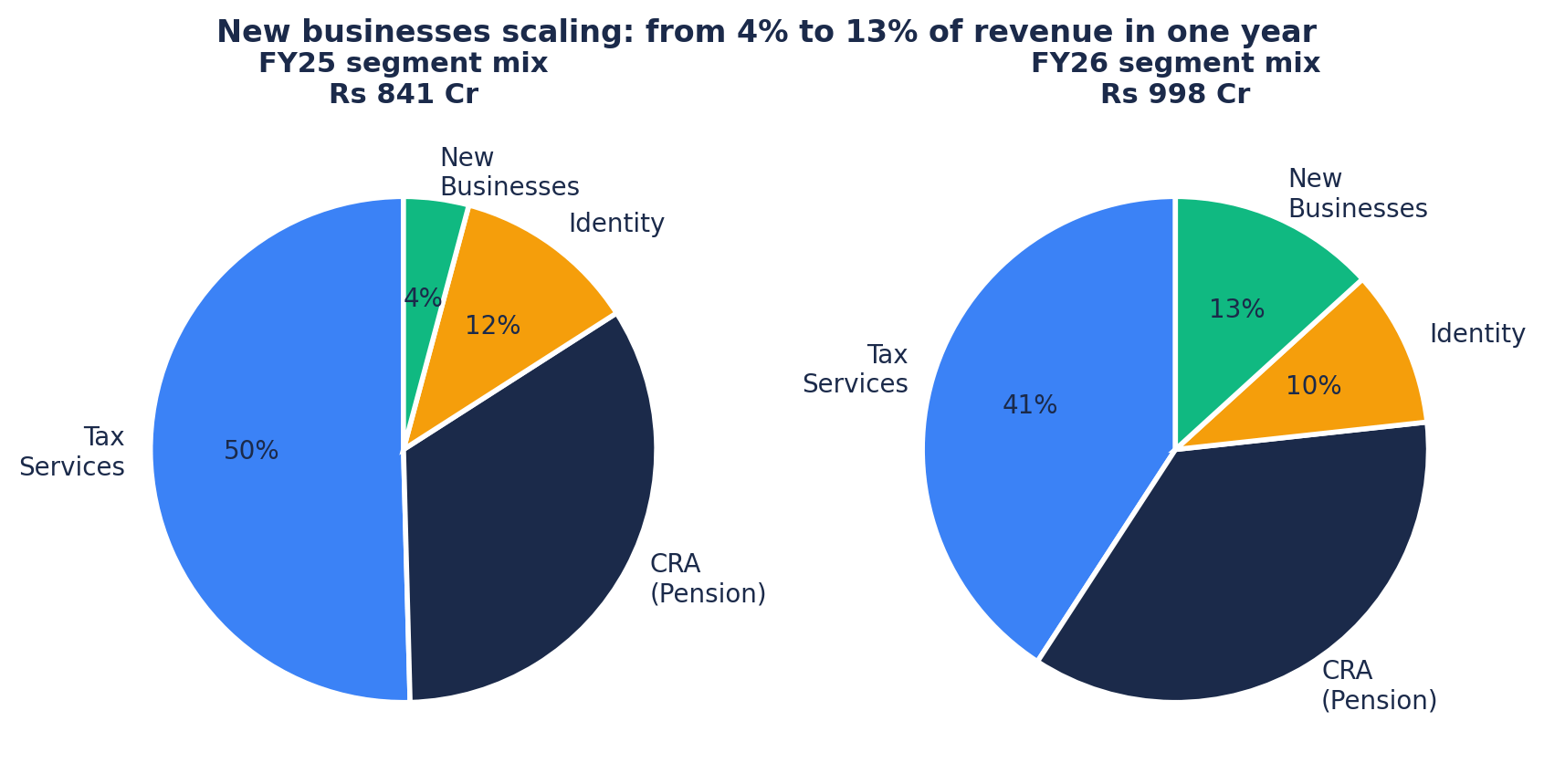

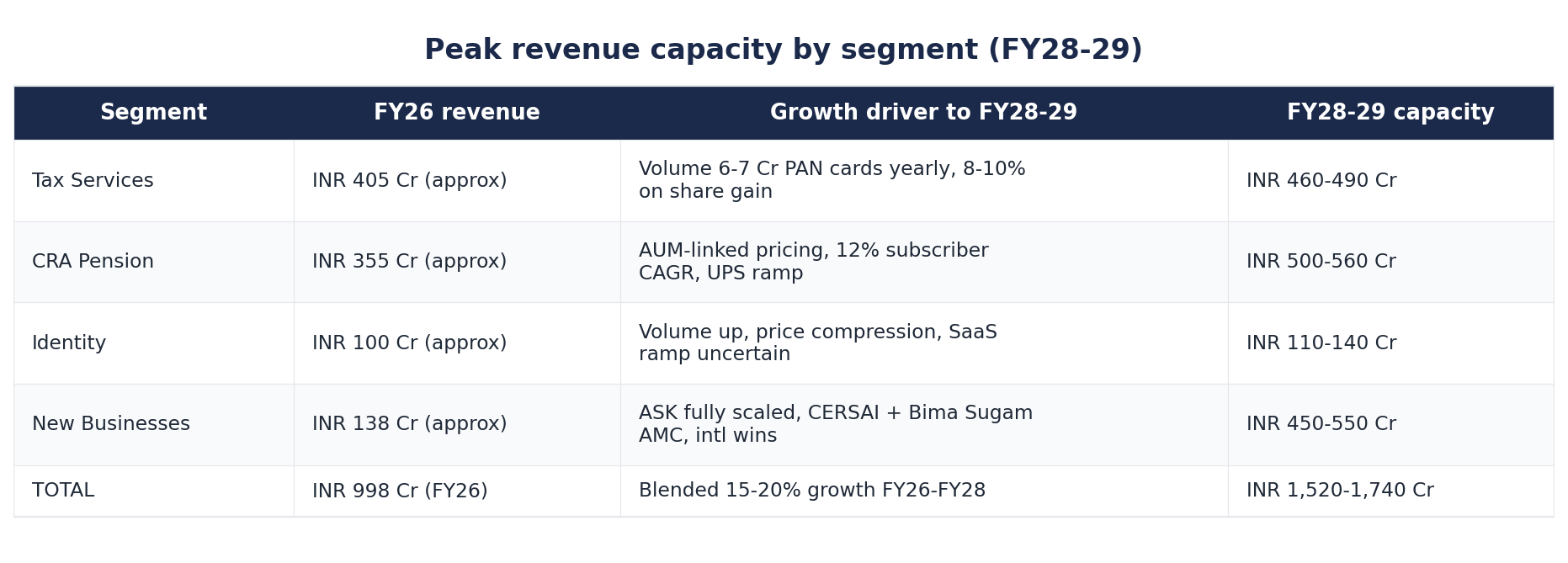

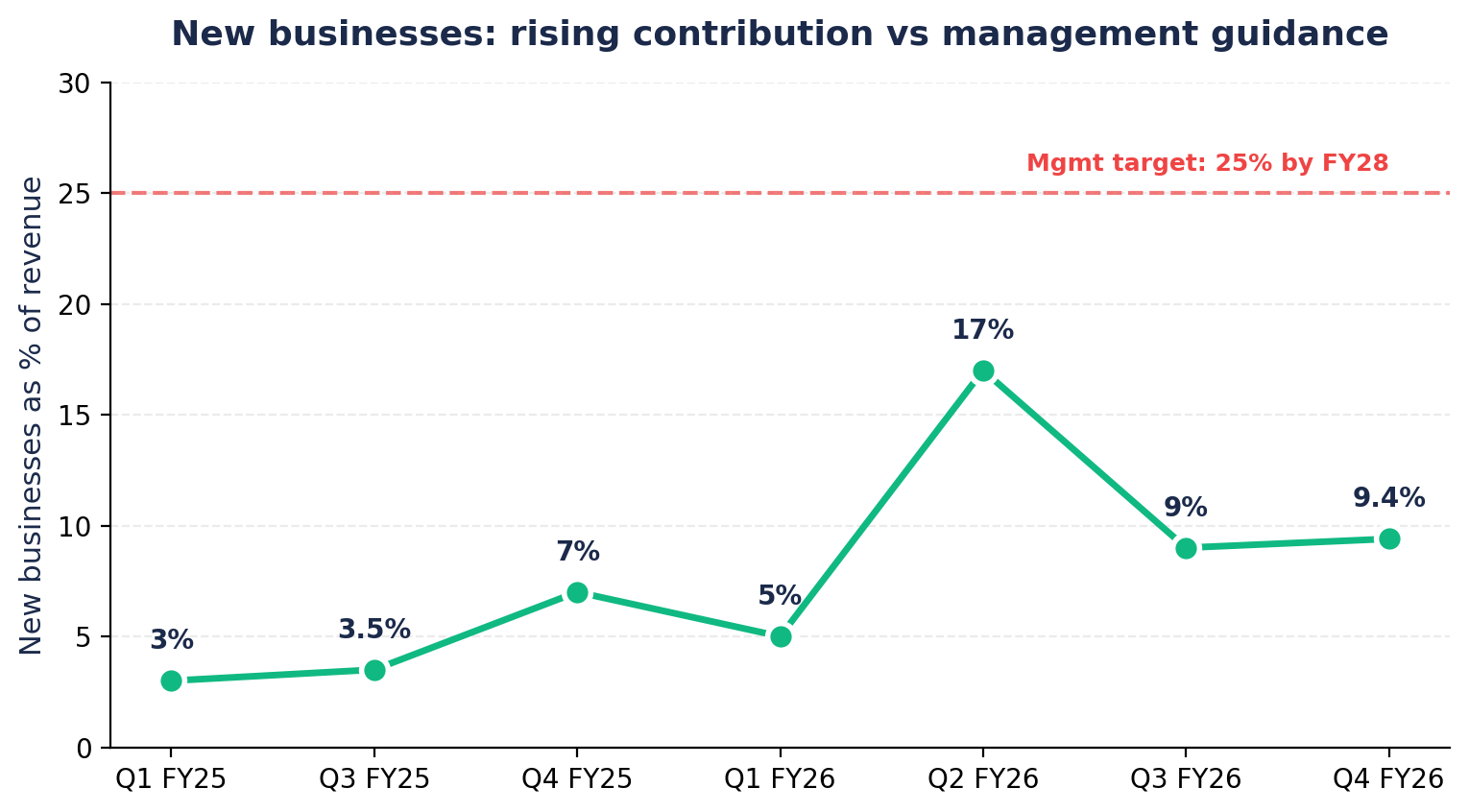

Protean reports four operating segments. As of FY26, the revenue mix is roughly 41% Tax Services, 36% CRA Services (Pension), 10% Identity Services, 13% New Businesses. The mix is shifting fast. New Businesses were 4% of revenue in FY25 and crossed 13% in FY26.

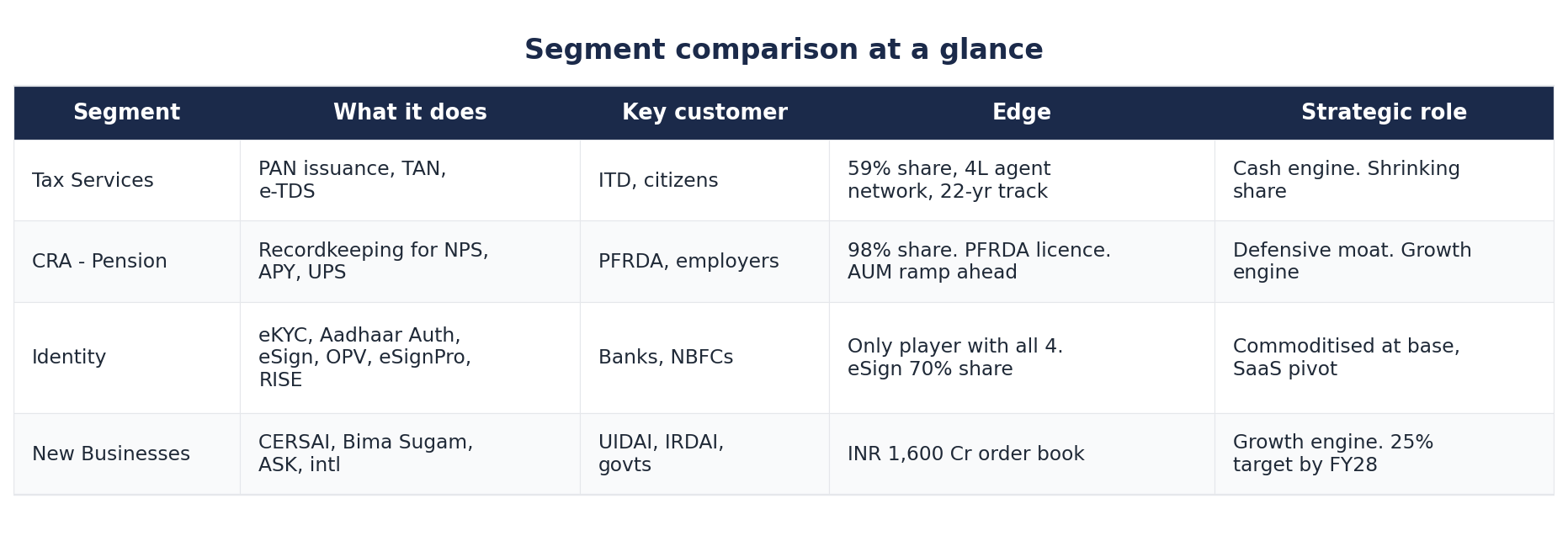

2.1 Tax Services (41% of FY26 revenue)

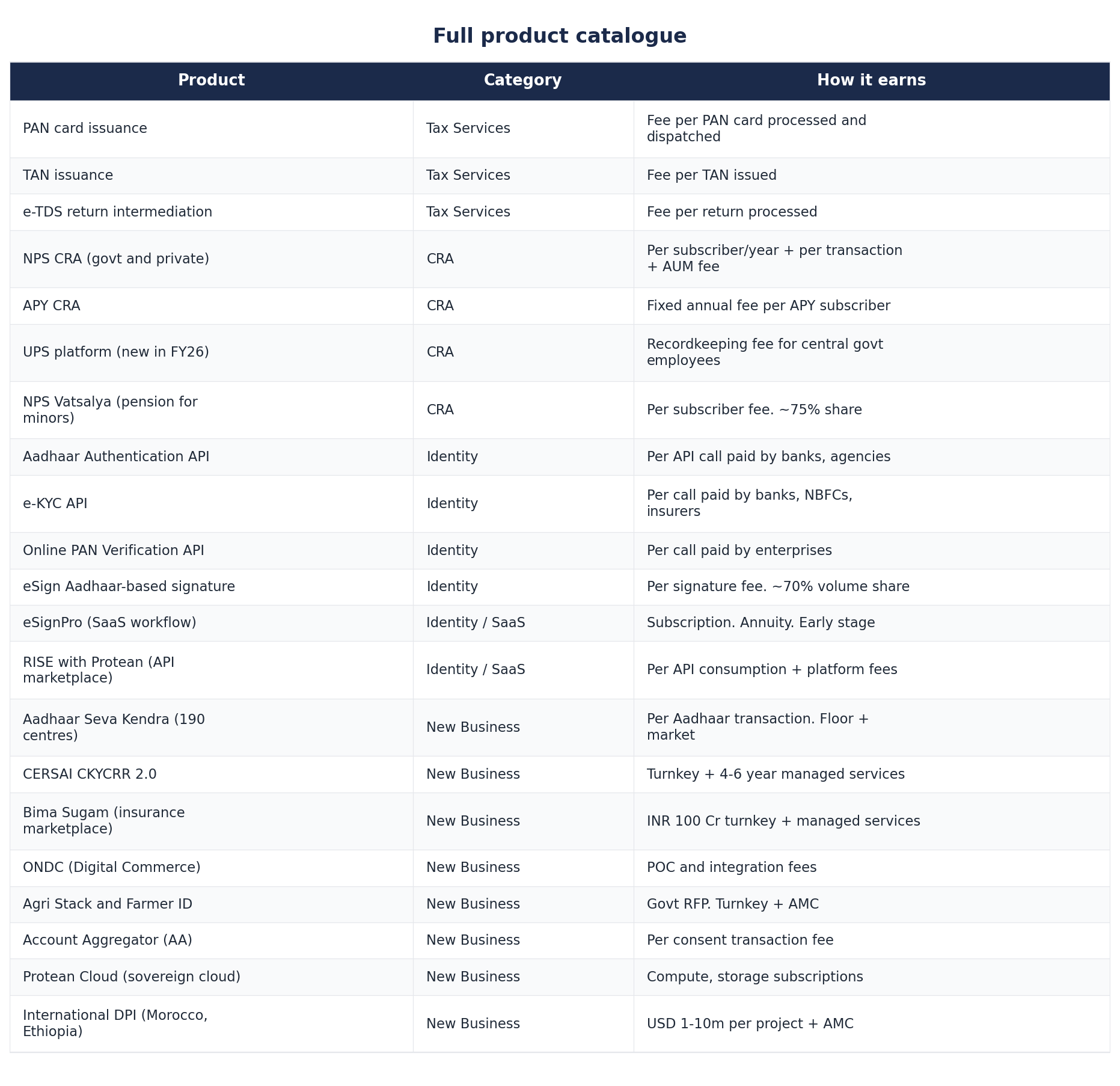

What it does. Protean operates the citizen-facing front-end of India’s PAN card system under a mandate it has held since 2003 from the Income Tax Department. It accepts PAN applications (paper and digital), conducts KYC validation, transmits clean data to ITD for PAN number allocation, and then prints and delivers the card. It also operates TAN (Tax Deduction Account Number) issuance, e-TDS return intermediation, and a few smaller allied services. The segment is purely transaction-priced: Protean earns a fixed fee per PAN card issued and a smaller fee on online PAN verifications and TAN/TDS transactions.

Core capability. Three things distinguish Protean: (1) a physical agent network of about 4 lakh touchpoints reaching into Tier 3, 4, 5 towns and rural India that no rival comes close to matching; (2) two decades of process knowledge in moving sensitive citizen data securely to ITD without identity leakage, audit failures or fraud; and (3) the ability to issue 4.4 crore PAN cards in a single year (FY25) without operational blowups.

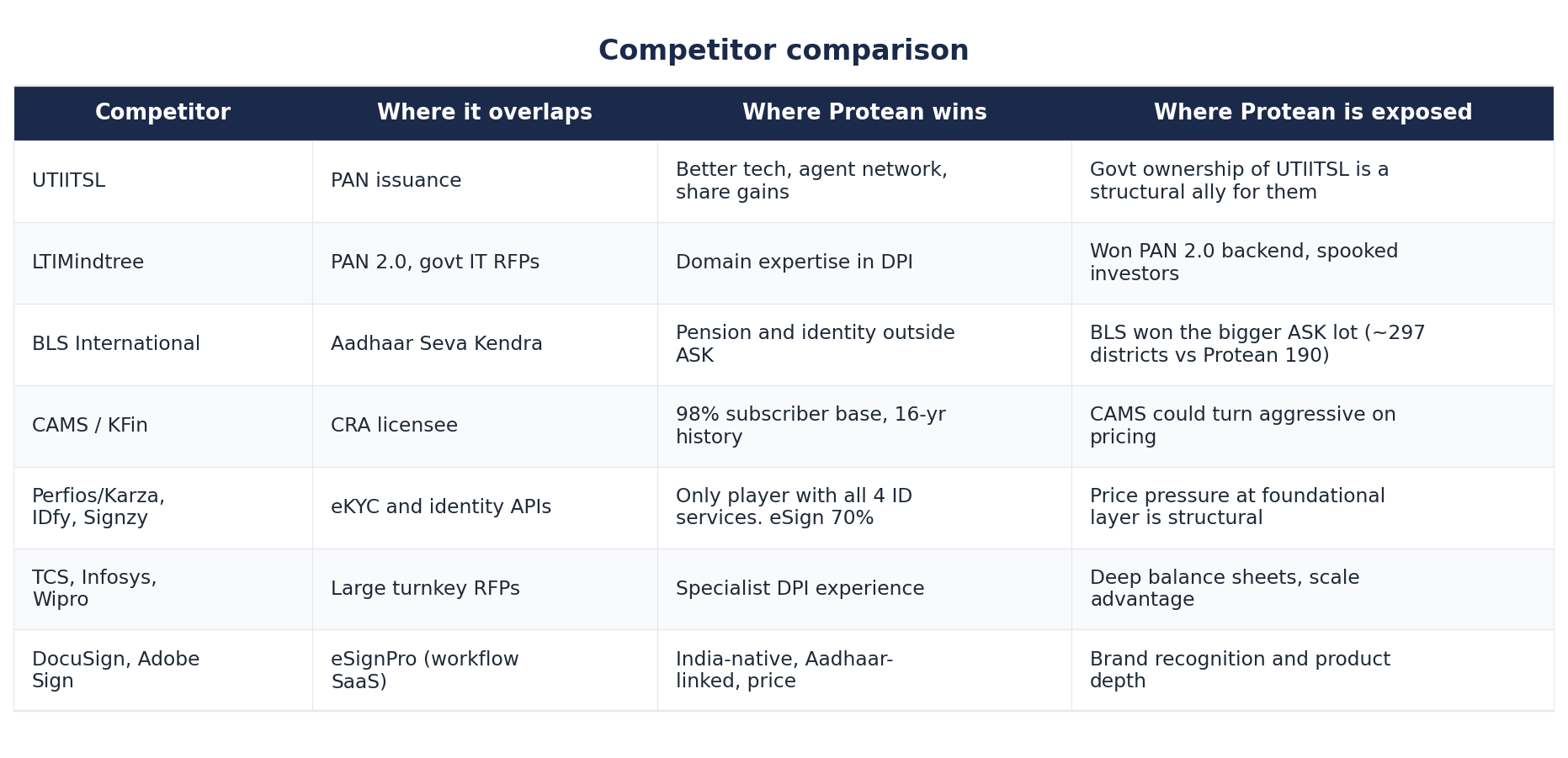

Competitive position. The market is essentially a duopoly between Protean and UTI Infrastructure Technology and Services Ltd (UTIITSL), a government-owned entity. In FY25, Protean held 56.6% market share; this rose to 59% in Q1 and Q2 FY26, and remained at about 59% through Q3 FY26. UTIITSL holds the rest. Each year, the country issues roughly 6-7 crore new PAN cards under normal conditions.

The PAN 2.0 overhang. In November 2024, the IT department announced PAN 2.0, a tech revamp of its internal allocation systems. LTIMindtree was awarded the contract in 2025. The market panicked, interpreting this as a threat to Protean’s PAN mandate. Management has spent the last four calls explaining that PAN 2.0 is a backend tech upgrade for the ITD systems (deduplication, allocation, storage) and is completely separate from Protean’s front-end mandate (application processing, KYC, card issuance, dispatch). Whether the market eventually accepts this framing depends on what direction the IT department takes once PAN 2.0 is fully deployed, which is at least two years away. We treat this as the single biggest risk to the segment.

How it fits in. Tax Services has historically been the cash engine. It generates the float that funds investments in Identity, New Businesses, and international expansion. As volumes plateau and PAN 2.0 uncertainty lingers, management is deliberately reducing its relative weight: 50% of revenue in FY25, 41% in FY26, and trending lower.

2.2 CRA Services - the pension recordkeeping business (36% of FY26 revenue)

What it does. Protean is the Central Recordkeeping Agency (CRA) for India’s National Pension System (NPS), Atal Pension Yojana (APY), and the newly launched Unified Pension Scheme (UPS) for central government employees. The CRA is the contractually licensed entity that keeps the record of every subscriber’s account.

Core capability and market share. Protean’s CRA has 98% of all cumulative NPS and APY subscribers (8.2 crore subscribers as of Q1 FY26). New subscriber additions have ranged from 32 to 41 lakh per quarter through FY26, with Protean capturing 94 to 98% of all new pension subscribers added. The only other CRA is Computer Age Management Services (CAMS), which got a CRA license later. In FY25, Protean became the primary CRA for UPS, the assured pension scheme for central government employees, which it built and deployed in record time.

Pricing structure. Historically, CRA revenue was a fixed transaction fee per subscriber, per contribution, per transaction. In Q3 FY26, PFRDA shifted the private-sector CRA pricing to a model more closely linked to assets under management (AUM). The intent is to incentivize the industry to grow pension AUM. In the short term, this compressed CRA revenue. Management calls it a one- to two-quarter re-base and expects revenue to grow faster than before once new pricing settles in, because NPS AUM is about INR 14 lakh crore today vs INR 75 lakh crore in mutual funds.

Why this segment matters. Pension penetration in India is about 6% of the population. In OECD countries, it is 70%. The government’s stated ambition is to take it to roughly 30 crore subscribers over the next three to five years, up from 8.2 crore today.

“Pension penetration in India is just 6% while if you look at most of the OECD countries, they are sitting at some 70% penetration. So, there’s a huge headroom over there.”

- Suresh Sethi, MD, Q2 FY26 concall, Nov 7, 2025

2.3 Identity Services (about 10% of FY26 revenue)

What it does. Identity Services is the API layer that banks, NBFCs, insurers, payment companies, and government agencies use to verify a citizen’s identity. Protean is the only company in India that offers all four foundational digital identity services: eKYC (electronic Know Your Customer using Aadhaar), Aadhaar Authentication (biometric or OTP verification), Online PAN Verification, and eSign (Aadhaar-linked digital signatures for documents). On top of these foundational APIs, Protean has built value-added products: eSignPro (a SaaS workflow for digital signing and stamping that competes with global products like DocuSign) and RISE with Protean (a multi-sector API marketplace for BFSI digital onboarding).

Competitive dynamics. The foundational identity space is intensely competitive and increasingly commoditized. The pricing is slab-based - bigger volume customers extract bigger discounts - and competitors include Karza Technologies (now Perfios), IDfy, Signzy, and many smaller players. Protean has historically been the infrastructure backbone (about 70% share of eSign by volume per management), but as price pressure mounts, the revenue does not grow in line with volume. Volumes were up year-on-year in every quarter of FY26, but identity revenue declined year-on-year in Q2, Q3, and Q4 FY26.

The strategic response. Protean is moving up the stack from API-level identity to workflow-level SaaS. eSignPro and RISE are billed as recurring annuity products with higher margins. Management guided in Q4 FY25 and Q1 FY26 that these would contribute meaningfully in FY26 onwards. Through Q3 FY26, the contribution had not yet been visibly large enough to call out separately. Whether this pivot works is one of the two or three central questions for the next three years.

2.4 New Businesses (13% of FY26 revenue, up from 4% in FY25)

What it contains. The New Businesses bucket is everything Protean does outside of legacy Tax, CRA, and Identity. It includes:

Large RFP-led turnkey government projects in adjacent DPIs like CERSAI CKYCRR 2.0 (an INR 200 Cr-ish revamp of India’s central KYC repository) and Bima Sugam (an INR 100 Cr mandate to build IRDAI’s digital insurance marketplace)

The newly won Aadhaar Seva Kendra (ASK) mandate from UIDAI is worth INR 1,370 crore over five years across 190 districts, which, when fully scaled, will generate INR 200 Cr of annual recurring revenue

International DPI projects in Morocco (education), Ethiopia (agriculture), and active discussions across Africa, the Middle East, and Southeast Asia

The Open Network for Digital Commerce (ONDC) implementation work for banks

Agri Stack (the central agriculture data platform)

Protean Cloud and InfoSec (a sovereign cloud offering)

Early-stage SaaS products (eSignPro, RISE)

Why does this segment exist separately? The revenue is project-based and lumpy. A large RFP win like Bima Sugam generates a chunk of design and deployment revenue over 12 to 18 months, then a smaller ongoing managed services revenue for 4 to 6 years. The ASK mandate is different: it is a steadier transaction-fee model once centers are operational. The economics also differ from those of the core annuity businesses: working capital is heavier, milestone billing creates revenue lumpiness, and margins are in the mid-teens.

How it fits into the group. Management has positioned New Businesses as the diversification away from Tax Services. The stated target across multiple concalls is for New Businesses to account for 25% of revenue over the next 2 to 3 years. At 13% of FY26 revenue, the company is roughly halfway there with three years to go. The company-wide order book of about INR 1,600 crore (nearly twice annual revenue) sits almost entirely in this segment.

Segment comparison at a glance

Section 3. Products and geographies

Full product catalog

(1) regulated platforms it operates under license;

(2) APIs sold by transaction volume to enterprises;

(3) SaaS workflow products; and

(4) turnkey government RFP deliverables.

Geographies

India. Protean is a pan-India business. PAN card issuance reaches every postal code. The pension subscriber base spans every state. The agent network is concentrated in Tier 2, 3, and 4 cities and rural India, where assisted onboarding is the norm. The Aadhaar Seva Kendras are spread across 190 districts in all the major states.

International. Until FY25, Protean had no international revenue worth calling out. In FY25, it won its first two mandates: an education DPI in Morocco and a health initiative in Ethiopia. In Q3 FY26, it added a third mandate: the agricultural DPI for Ethiopia, valued at INR 25 crore. Management has spoken of active discussion with 20+ countries across Africa, the Middle East, and Southeast Asia.

Notable milestones

1995: Incorporated as NSDL e-Governance Infrastructure Ltd

2003: Awarded PAN processing mandate by the Income Tax Department

2009: Became the first CRA for NPS

2015: Atal Pension Yojana launched; Protean became the primary CRA

2022: Demerger from NSDL group; rebranded to Protean eGov

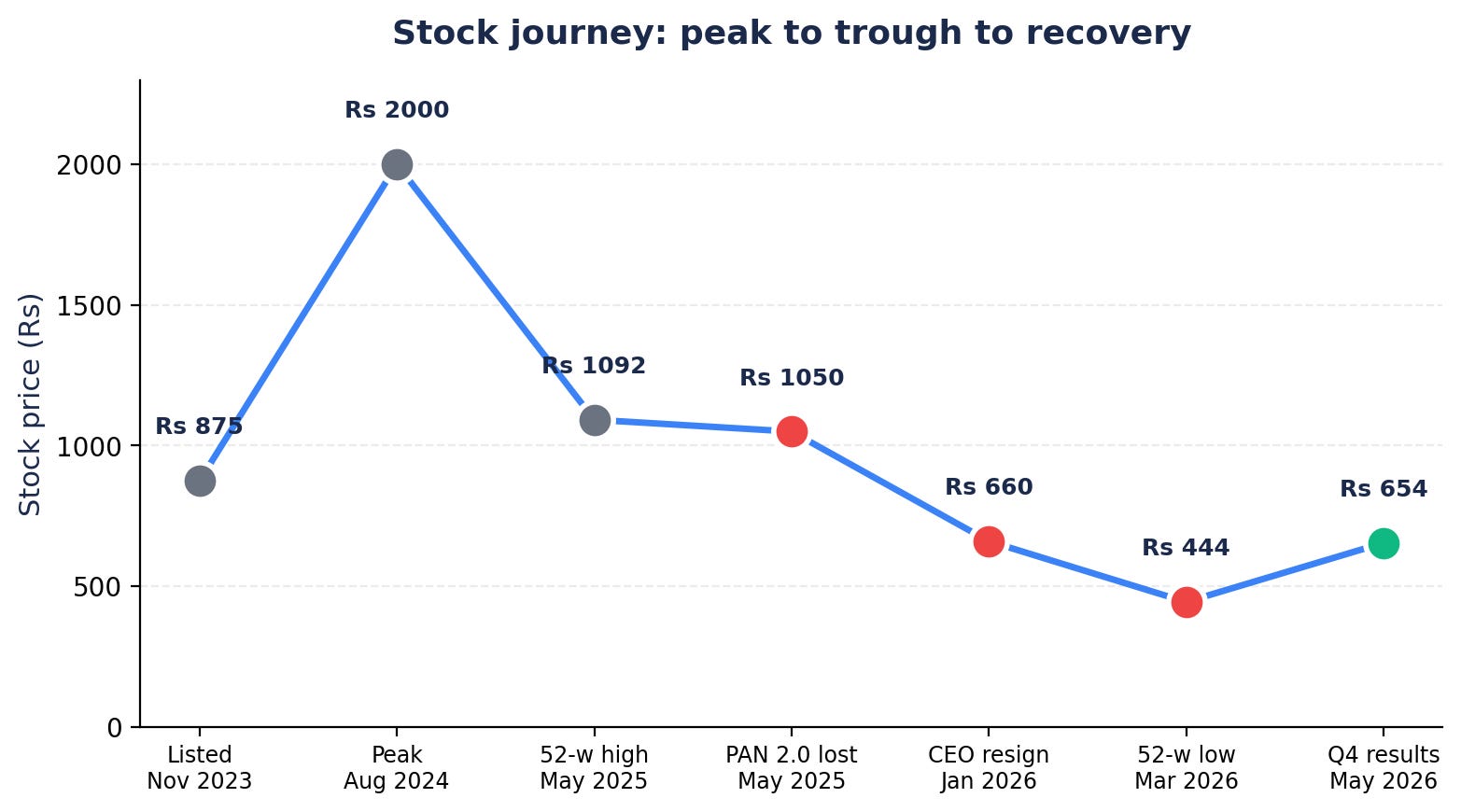

Nov 2023: IPO at issue price of INR 792, BSE and NSE listing

FY25: Won CERSAI CKYCRR 2.0, Bima Sugam, Morocco, and Ethiopia mandates

Apr 2025: Launched UPS in record time as primary CRA

Aug 2025: Won INR 1,370 Cr Aadhaar Seva Kendra mandate from UIDAI

Q3 FY26 (Feb 2026): Acquired 4.95% in NSDL Payments Bank for INR 30.2 Cr

Feb 27, 2026: NCLT approved the demerger of Protean Infosec into the parent

May 20, 2026: Q4 FY26 results, 38% YoY revenue growth, MD succession announced

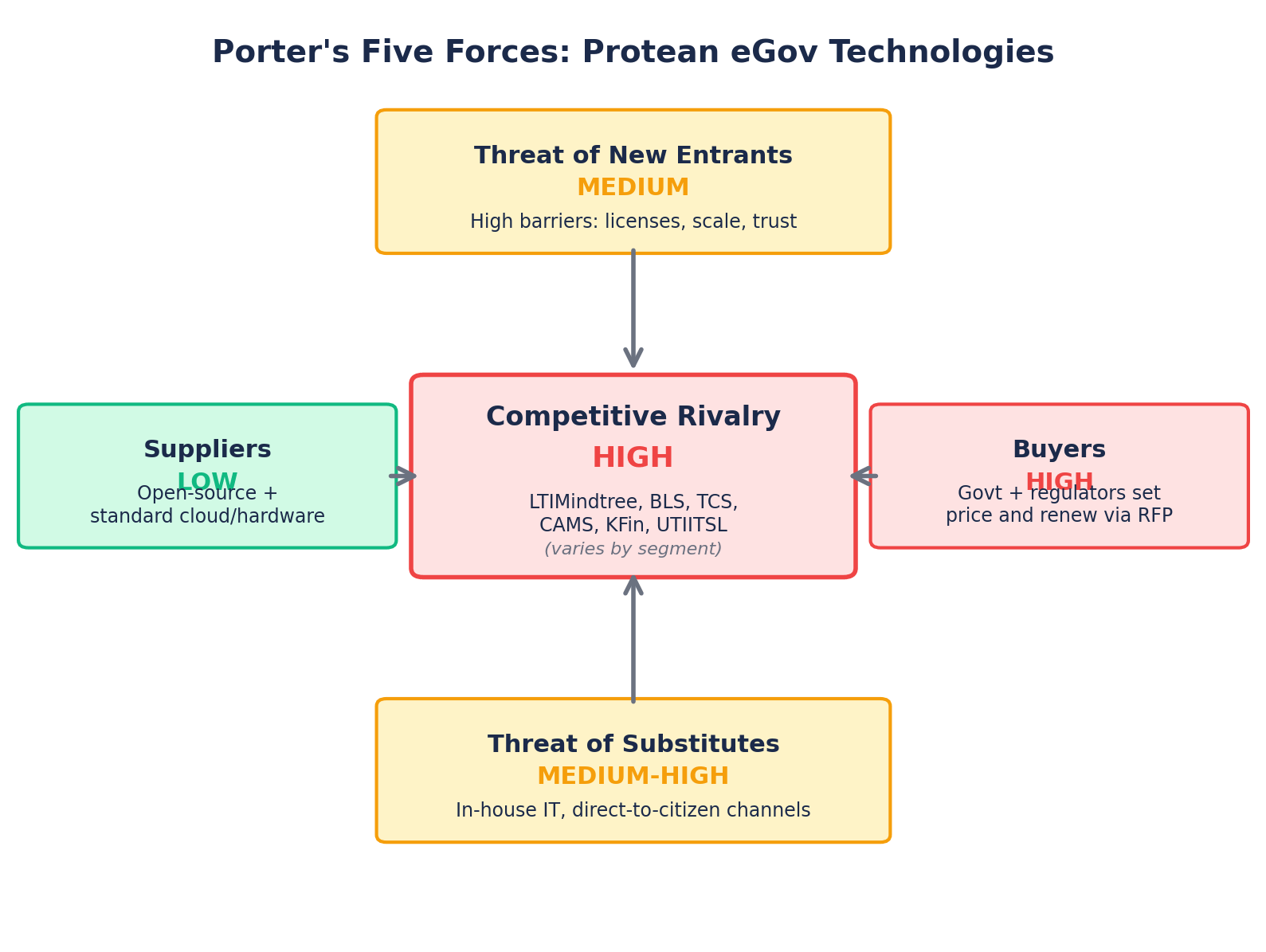

Section 4. Porter’s Five Forces

4.1 Bargaining power of buyers: HIGH

Protean’s largest customers are the Government of India and its regulatory arms: the Income Tax Department, UIDAI, PFRDA, IRDAI, and CERSAI. These are buyers of last resort: there is no other Income Tax Department to sell to. Each contract is awarded via RFP, and the government structures bids to drive prices down and renews them on its schedule. In Q3 FY26, PFRDA unilaterally restructured CRA pricing for the private sector pension business. Protean had no real ability to negotiate. Banks and NBFCs that buy identity APIs have lower bilateral leverage individually, but as a group, they have driven slab-based pricing that compresses Protean’s per-call realization as volume grows. Buyer power is HIGH and is the single most uncomfortable force in this business.

4.2 Bargaining power of suppliers: LOW

Protean’s main inputs are commodity cloud compute, networking, and software talent. The company runs its own sovereign cloud (Protean Cloud), uses open-source technology stacks, and has built a center of excellence with 400-plus open-source engineers. None of the inputs is sourced from a single supplier with pricing power. Supplier power is LOW.

4.3 Threat of new entrants: MEDIUM

The licensed businesses (CRA, eSign authentication, KYC) face very high entry barriers because regulators must be convinced of the entrant’s operational reliability, security, and balance sheet, and the application process typically takes a year or more.

The newer DPI businesses have lower entry barriers: well-funded tech services players like TCS, Infosys, Wipro, or LTIMindtree can bid on the same RFPs. They have deep balance sheets, fully scaled execution teams, and existing government relationships. Identity APIs arguably have the lowest barriers, which is why pricing has become commoditized. Net effect: MEDIUM.

4.4 Threat of substitutes: MEDIUM-HIGH

The dangerous substitute for Protean is the government deciding to insource the work entirely. This is exactly what PAN 2.0 looks like in part - the IT department asked the market to build the tech stack that ITD itself would operate, bypassing Protean’s current intermediary role. A second substitute is direct-to-citizen digital channels, such as the IT department’s e-filing portal: as more citizens become comfortable applying for a PAN online, the agent-assisted channel that Protean dominates becomes less necessary. Today, about 70% of applications are still assisted, but that share has been drifting down. Substitute risk is MEDIUM-HIGH.

4.5 Competitive rivalry: HIGH

Within each segment, Protean faces specific named rivals:

Tax Services: UTIITSL is the only other PAN issuer. Effectively a duopoly

CRA Pension: CAMS holds the second CRA license but has a tiny share. Protean is dominant

Identity: Karza (Perfios), IDfy, Signzy, Digio, e-Mudhra. Crowded and price-competitive

Bima Sugam, CERSAI, ASK turnkey RFPs: Faces TCS, Wipro, LTIMindtree, Tech Mahindra, BLS International (BLS won the larger 297-district ASK lot)

SaaS workflow products: DocuSign, Adobe Sign, Leegality, Signzy in eSign workflow

International DPI: Globally faces system integrators and the rare specialized DPI consultants

Protean operates in industries with asymmetric force profiles. The licensed core (CRA, PAN) has high barriers but also a single powerful buyer who can change the rules unilaterally (as PFRDA did in Q3 FY26). The newer growth areas have lower barriers but more fragmented buyers and intense price rivalry. Protean's defense is to climb the value chain into SaaS, where switching costs and differentiation are higher. Whether it can complete that climb fast enough is the open question.

Section 5. Future Tracks

Protean is structurally an asset-light business: there are no plants, no inventories, no heavy capital cycles. Capex flows in three tracks.

5.1 Track one: technology and IP capex

Through FY23, FY24, and FY25, the company built proprietary technology stacks for its newer businesses: the eSignPro workflow platform, the RISE API marketplace, Protean Cloud (the sovereign cloud product), the ONDC implementation, the Agri Stack consent and data sharing modules, and the DPI in a Box framework. This shows up as intangible asset additions plus accelerated amortization in FY25. Management has indicated that depreciation will remain at 4.5-5.5% of revenue going forward.

5.2 Track two: Aadhaar Seva Kendra infrastructure

The single biggest physical capex underway is the ASK rollout. Each center needs leased premises, biometric capture devices, networked computers, signage, security, staff training, and ongoing operations. Management has not publicly disclosed the per-center setup cost. Based on industry comparables, we estimate INR 25 to 40 lakh setup capex per center, implying a total upfront investment of INR 50 to 75 crore for all 190 centers.

5.3 Track three: working capital for RFP execution

Large RFP-based projects such as Bima Sugam, CERSAI, and ASK use milestone billing. Protean incurs salary and system costs throughout the year, but client receipts come in chunks against milestones. This is why Sandeep Mantri has repeatedly described the INR 800-850 crore in cash on the balance sheet as a working-capital cushion for new-business execution rather than excess capital to be returned.

5.5 The cash on the balance sheet

Protean carries about INR 850 crore in cash and marketable securities (as of March 31, 2026). Market cap at the post-Q4 FY26 result share price of about INR 648 on NSE is approximately INR 2,665 crore. Cash is therefore about 32% of market cap. The company has been debt-free for years. Management has repeatedly said the cash is earmarked for (a) working capital to deliver large RFP projects and (b) selective inorganic acquisitions, with NSDL Payments Bank stake (INR 30.2 Cr in Q3 FY26) as the first move. Buybacks have been explicitly ruled out by the CFO in the Q3 FY26 concall.

Section 6. Industry: demand drivers, size, regulation

What industry is Protean in?

Protean sits at the intersection of three industries: (1) Digital Public Infrastructure (DPI) services; (2) BFSI technology infrastructure; and (3) IT-enabled services more broadly. None of these is a clean category that maps to a published industry size.

Demand drivers

Working-age population growth at about 1.0-1.2% per annum. Each new entrant to the workforce eventually needs a PAN card, often a pension account, and increasingly an Aadhaar-linked identity verification trail.

Tax base expansion. India had about 9.4 crore income tax filers in AY25. PAN penetration is around 40% of the population.

Pension penetration ramp. 6% of Indians have pension coverage today vs 70% in OECD. NPS Vatsalya, UPS, and the expansion of the Atal Pension Yojana are all designed to widen the funnel.

Financial inclusion and KYC volume. Every new bank account, NBFC loan, and insurance policy creates a KYC event. Industry-wide KYC volumes have grown about 25% per year.

Government insistence on DPI for every sector. The India Stack template is being applied to healthcare, agriculture, education, insurance, credit, and commerce.

India Stack export. The G20 DPI Task Force and India Stack Global Program have positioned India’s templates as exportable to other developing countries.

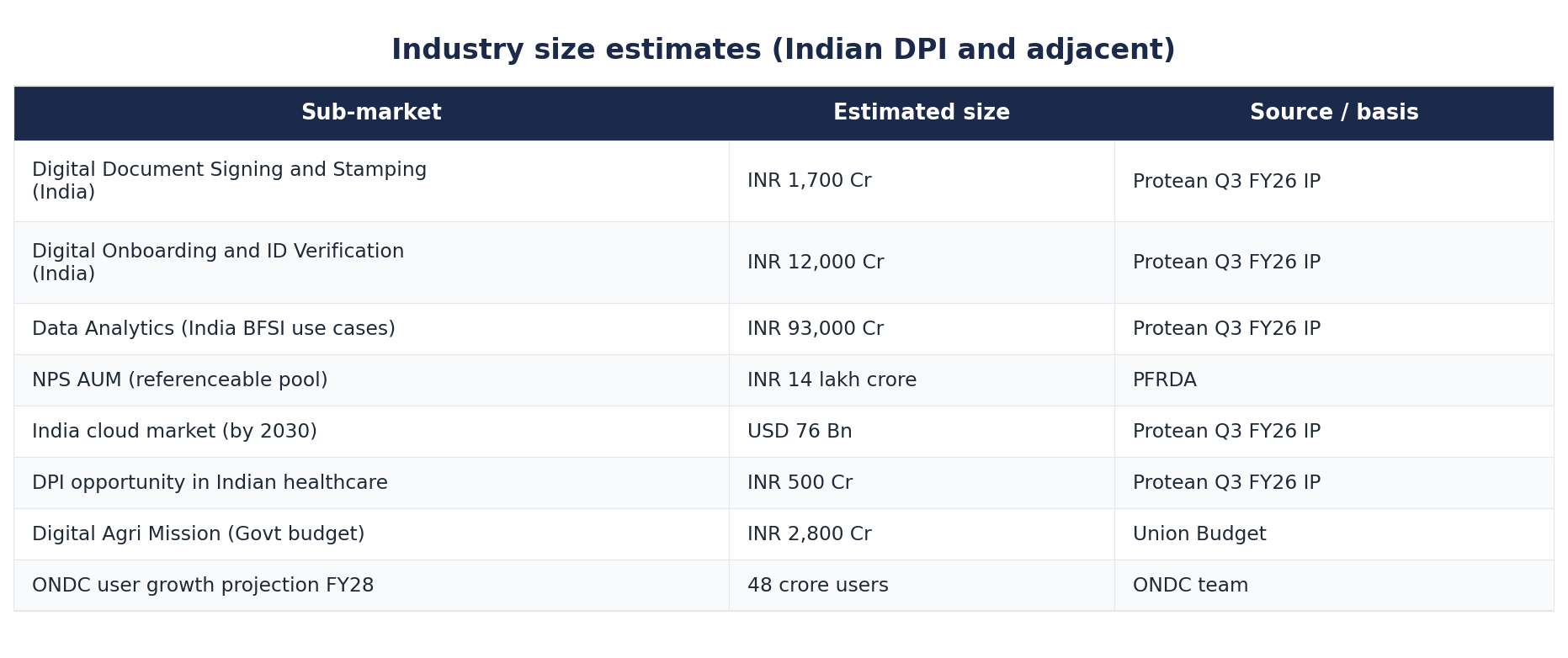

Industry size estimates

Where India sits in the global supply chain

India built the world’s largest unified ID system (Aadhaar, 1.4 billion identities) and arguably the most adopted real-time payments system (UPI). On the back of this, Indian DPI specialists have an international credibility advantage. Protean, by virtue of running the PAN, CRA, and identity rails, is one of a very small group of Indian companies that can credibly bid to build similar systems abroad.

Regulatory environment

Protean is regulated by multiple authorities depending on the service. PFRDA licenses the CRA business. UIDAI licenses Aadhaar Authentication and eKYC. The CCA (under MeitY) licenses eSign service providers. The Income Tax Department directly contracts the PAN issuance work. CERSAI, IRDAI, and RBI are buyers/regulators for newer mandates. The DPDP Act (Digital Personal Data Protection Act, enacted in 2023) puts obligations on data fiduciaries that directly affect how Protean handles citizen data.

Cyclicality

Most of Protean’s revenue is non-cyclical. PAN issuance is driven by structural factors (formalization, new schemes) rather than GDP cycles. Pension subscriber additions track government policy rather than economic mood. Identity API volume tracks BFSI lending volume, which is cyclical but structurally growing.

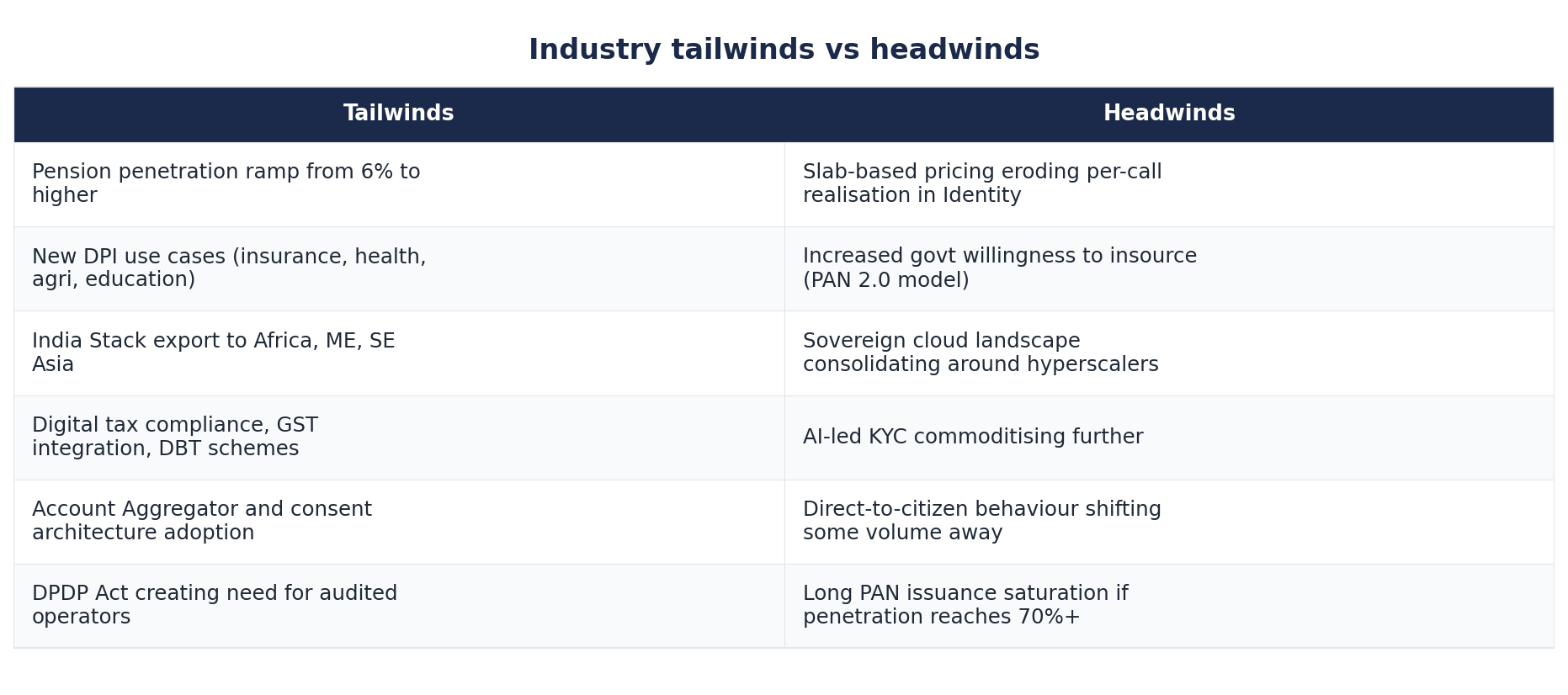

Tailwinds and headwinds

Section 7. Key catalysts and earnings triggers

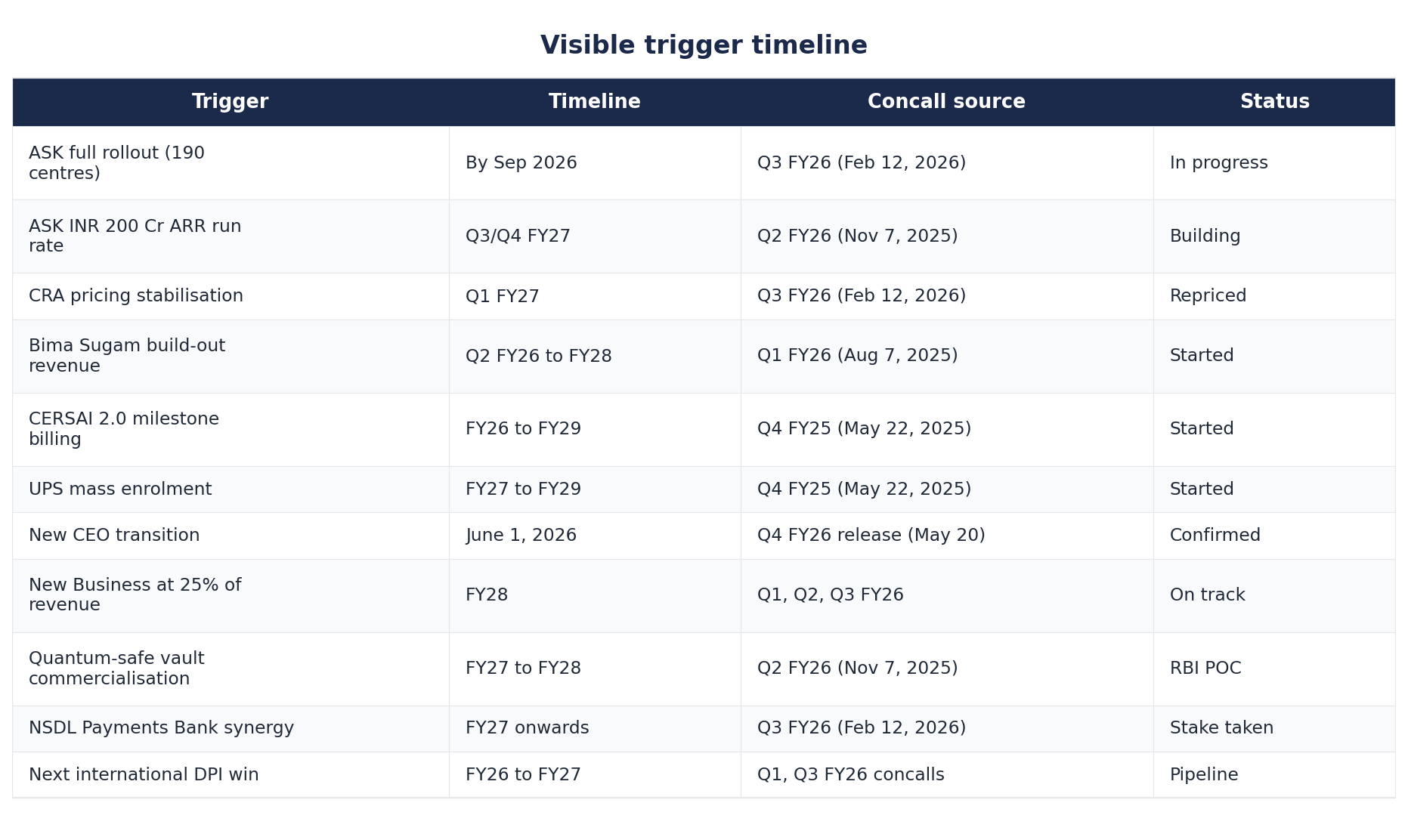

Every trigger below is sourced directly from one of the four concall transcripts on file (Q4 FY25 May 22 2025, Q1 FY26 Aug 7 2025, Q2 FY26 Nov 7 2025, Q3 FY26 Feb 12 2026) or from the Q4 FY26 results press release dated May 20, 2026. Forward-looking only.

Tier 1: visible triggers in the next 12 to 18 months

Aadhaar Seva Kendra full rollout to all 190 centers by Sep 2026. Management said in Q3 FY26 (Feb 12, 2026): all 190 centers will be operational by Sep 2026. Full revenue impact visible from Q3/Q4 FY27 onwards. Adds INR 200 Cr of ARR at peak (Q2 FY26 concall, repeated Q3 FY26).

CRA pricing normalization after PFRDA’s Q3 FY26 restructuring. Sandeep Mantri said, “I think it will take one more quarter and the prices will stabilize.” Q3 FY26 concall, Feb 12, 2026.

CERSAI CKYCRR 2.0 revenue ramp. Management said in Q1 FY26 (Aug 7, 2025) that revenue starts kicking in from Q2 onwards. In Q3 FY26, they confirmed that CKYCRR revenue was recognized in Q2 and Q3.

Bima Sugam build-out revenue. INR 100 Cr mandate won in Q1 FY26 (Aug 7, 2025). Revenue contribution from Q2 FY26 onwards, peaking in FY27.

UPS subscriber onboarding ramp. Built and deployed on April 1, 2025. 19,000 accounts onboarded by June 30, 2025.

Ethiopia agriculture DPI - INR 25 Cr. Won in Q3 FY26 (Feb 12, 2026). Revenue spread over 2-3 years.

Ajay Rajan takes over as MD and CEO from June 1, 2026. Announced May 20, 2026, with Q4 results. Suresh Sethi departs after a personal decision.

Tier 2: medium-term triggers (18 to 36 months)

Move to 25% revenue contribution from New Businesses. Currently 13%. Targeted by FY28. Reaffirmed by Sandeep Mantri in Q1, Q2, and Q3 FY26 concalls.

AUM-linked pricing benefit in CRA. Suresh Sethi, Q3 FY26: “As AUM grows, you will see an improvement in the pricing structure.” NPS AUM at INR 14 lakh crore today.

eSignPro and RISE with Protean scaling to material revenue. Sandeep Mantri, Q1 FY26: “In the next 3 years, we should see strong revenues coming out of a couple of these products.”

International order pipeline conversion. Suresh Sethi, Q3 FY26: 4 international mandates across 3 markets. “Multiple discussions, last stages of evaluation” in Africa, the Middle East, and Southeast Asia.

NSDL Payments Bank partnership monetization. 4.95% stake acquired for INR 30.2 Cr in Q3 FY26.

NPS subscriber base widening to 30 crore. Suresh Sethi, Q2 FY26: “The ambition is really to grow it up to 30 crore subscribers in the matter of next 3 to 5 years” from 8.2 crore today.

Quantum-safe data vault and AI-in-a-box. Unveiled at GFF 2025. White paper under RBI evaluation.

Tier 3: long-term option value

Protean Cloud as a sovereign cloud play. India’s cloud market is projected at USD 76 Bn by 2030.

Sale of stake in NSDL Payments Bank as the bank scales. Optionality on the 4.95% holding.

Data analytics platform monetization for BFSI (INR 93,000 Cr opportunity).

DPI export is accelerating with backing from the India Stack Global Program.

PAN 2.0 outcome is turning out to be neutral or positive as the framework is defined.

Visible trigger timeline

Section 8. Key risks

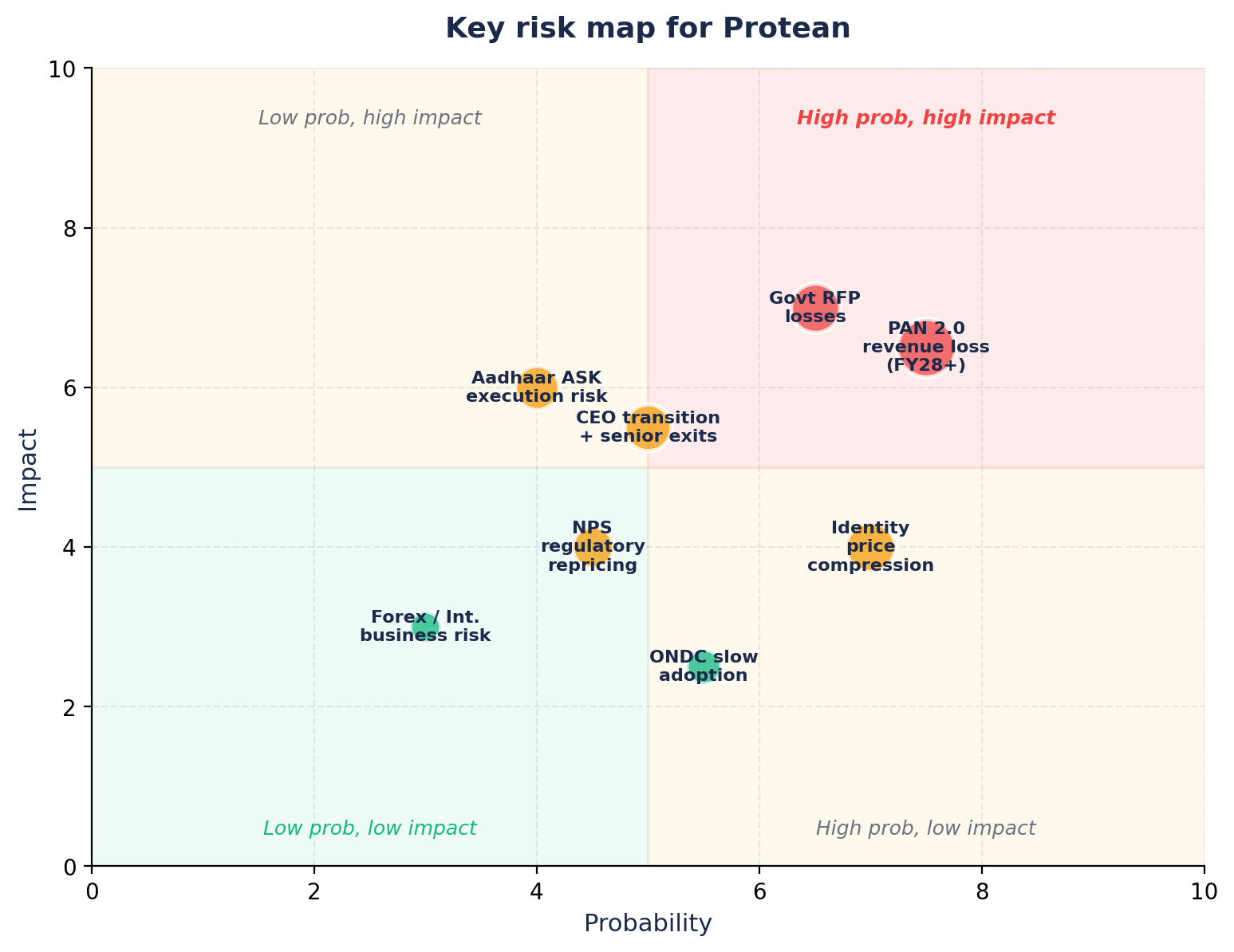

8.1 PAN 2.0 ambiguity (HIGH likelihood, HIGH impact in worst case)

Mechanism. The IT department awarded the PAN 2.0 backend tech stack revamp to LTIMindtree in 2025. The published RFP language suggests the new system will consolidate “end-to-end PAN servicing starting from online receipt, verification, deduping, and processing allotment.” Protean’s management argues that its front-end processing and citizen distribution mandates are separate. If that interpretation is right, the impact on Protean is neutral. If the government eventually decides to consolidate distribution as well, Protean would lose its largest single revenue line. Tax Services was 41% of FY26 revenue.

Calibration. The base case is that the duopoly with UTIITSL will continue for 2 to 4 more years, given the political and operational complexity of disrupting citizen access. Worst case is that direct-to-citizen channels accelerate post-PAN 2.0 deployment, and Protean’s volume drifts down by 5 to 8% per year from FY28 onwards.

“So, the digital opportunity to apply directly exists even as we speak today. But the choice of the citizens is clearly more tilted towards going through an assisted model. So that is the reason we are saying that these things do not change overnight.”

- Suresh Sethi, Q4 FY25 concall, May 22, 2025

Today, only Chat GPT has launched Form Filler

https://decrypt.co/331756/chatgpt-agent-book-browse-fill-forms-just

Citizens were not interested in filling out the form because it was painful to complete such a long one. Now, with AI, you can easily fill out the form. This could be the biggest tailwind for this stock

8.2 PFRDA unilateral pricing reset risk (MEDIUM likelihood, MEDIUM impact)

Mechanism. In Q3 FY26, PFRDA shifted CRA pricing to an AUM linkage. The transition was evident in CRA revenue compression that quarter, despite subscriber growth. The regulator has structural objectives that may not align with CRA profitability in any given quarter. Future rate resets are entirely the regulator’s call.

Calibration. The CFO calls this temporary (1-2 quarters). The AUM tailwind is real and continues to grow over time. But the precedent is set: PFRDA can change the rules, and Protean has no negotiating leverage.

8.3 Identity Services margin death spiral (HIGH likelihood, LOW-MEDIUM impact)

Mechanism. Foundational identity APIs are commoditizing. Volume grew across all four facets every quarter through FY26, yet revenue declined year-on-year in Q2, Q3, and Q4 FY26. The SaaS pivot (eSignPro, RISE) is supposed to offset this, but as of Q3 FY26, the company refused to break out customer counts for these products.

Calibration. Identity is about 10% of revenue, so even a 20% miss is a 200 bps top-line drag. Limited margin impact because the segment is already low margin. A bigger concern is what this tells us about the company’s ability to monetize SaaS in general.

8.4 ASK execution risk (MEDIUM likelihood, MEDIUM impact)

Mechanism. The 190-center Aadhaar Seva Kendra mandate is Protean’s first large physical operations build in years. As of Q3 FY26, only 34 centers were live, meaning roughly 80% of the rollout must be completed in the next 6 months (target: Sep 2026). Slippage would push the INR 200 Cr ARR revenue impact from FY27 into FY28. Operational issues at scale (queue management, system uptime, refund handling) could also create reputational damage.

8.5 Senior management exit and succession (MATERIALISED, MEDIUM impact)

Mechanism. Suresh Sethi has been the MD and CEO for several years and the public face of the company across every concall. On May 20, 2026, the board announced that Ajay Rajan will take over as MD and CEO from June 1, 2026. The CFO Sandeep Mantri stays. Beyond the CEO, Q3 FY26 (Feb 12, 2026) acknowledged several other senior exits, attributed to retirement and restructuring.

“We’ve got, as earlier mentioned, a strong leadership in place across all the verticals as we had restructured the organization sometime last year. And there is absolute continuity, and we don’t see any disruption.”

- Suresh Sethi, Q3 FY26 concall, Feb 12, 2026

Calibration. Sethi led the company through the IPO, the demerger from NSDL and several large RFP wins. The risk is that execution slows during the transition or that strategic direction shifts. Markets typically discount such transitions for 2 to 3 quarters.

8.6 Other income dependency (LOW likelihood of issue, but worth flagging)

Mechanism. Protean carries about INR 850 crore of cash and marketable securities. Treasury income for this pool is sizeable: in FY25, other income was INR 68 crore, against an operating EBITDA of INR 80 crore. Reported EBITDA at INR 149 crore is therefore propped up by treasury yield. Pure operating EBITDA in FY25 was about INR 80 crore (10% of sales). One investor in the Q1 FY26 concall called this out explicitly.

Calibration. Not a going concern risk. But makes the underlying business margin look better than it really is.

8.7 Demerger of Protean Infosec (MATERIALISED, NEUTRAL impact)

Protean filed for the demerger of its 100% subsidiary Protean Infosec Services Ltd into the parent. NCLT approved the demerger on Feb 27, 2026. Net impact is operational consolidation. No red flag.

8.8 Concentration risk in government revenue

Protean’s largest single customer relationships are with the IT department (PAN), PFRDA (CRA), UIDAI (ASK), and IRDAI (Bima Sugam). Together, these government-related counterparties account for the majority of revenue. There is no single private customer that comes close. This is both a strength (sticky, regulated, deep) and a concentration risk.

Section 9. Walk the talk: management credibility

This section cross-references what Protean management said across the four concalls against what actually happened.

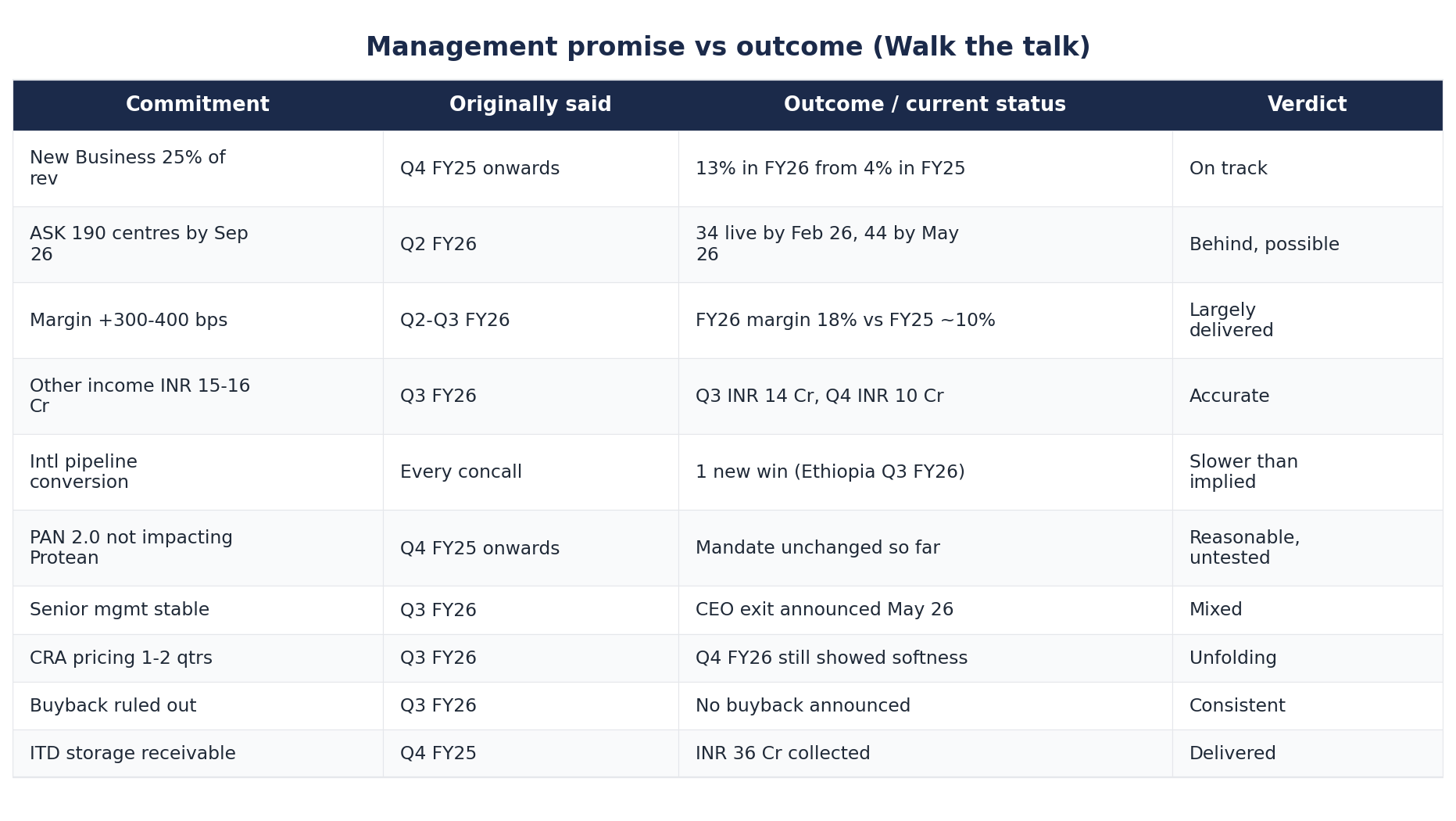

Promise 1: New Businesses to be 25% of revenue in 2-3 years

“What we are saying is basically our core businesses... will grow somewhere between 8% and 12%, and our new businesses will contribute 25% to 30% in the next three years.”

- Sandeep Mantri, Q4 FY25 concall, May 22, 2025

This statement was reiterated in Q1 FY26 (Aug 7, 2025), Q2 FY26 (Nov 7, 2025), and Q3 FY26 (Feb 12, 2026). New Businesses grew from 4% of revenue in FY25 to 13% in FY26. The company is roughly halfway to the 25% target with two and a half years on the clock. Verdict: On track, ahead of an internal extrapolation.

Promise 2: ASK rollout completion by September 2026

“As per the mandate, Protean has to roll out 190 centres, out of which 34 are already rolled out in this quarter. By September, we should be able to roll out everything.”

- Sandeep Mantri, Q3 FY26 concall, Feb 12, 2026

ASK was won in August 2025. By Q3 FY26 (Feb 2026), 34 centres operational. By the Q4 FY26 result release (May 20, 2026), the tally is at least 44. 80% of centres remain to be opened in 4 months. Verdict: Behind schedule if straight-lined, but the back-end of the rollout is faster. To watch every quarter.

Promise 3: Margin expansion of 300-400 bps over the next couple of years

“EBITDA, we are already at 19%, if you see. So, there will be an expansion of 300 to 400 basis points, which is what we said last time also in next couple of years once we start growing our revenues at this stage.”

- Sandeep Mantri, Q3 FY26 concall, Feb 12, 2026

Reported EBITDA margins by quarter in FY26: Q1 18.8%, Q2 16.6%, Q3 19% (adjusted), Q4 about 17%. Full year FY26 EBITDA at INR 188 Cr is 18% of revenue. Margin already at the lower end of the guided range. Verdict: Reasonable trajectory, not yet fully delivered. Test is FY27.

Promise 4: Treasury income of INR 15-16 Cr per quarter

“Normally, other income is steady at INR 15 to 16 crores level.”

- Sandeep Mantri, Q3 FY26 concall, Feb 12, 2026

Other income by quarter in FY26: Q1 INR 29 Cr (high), Q2 INR 15 Cr, Q3 INR 14 Cr, Q4 INR 10 Cr. Treasury baseline holds at roughly the guided level. Verdict: Honest and accurate.

Promise 5: International order pipeline conversion

“We are still in advanced stage of negotiation for a few RFPs. Still, we have not received any major wins apart from the ones announced earlier.”

- Sandeep Mantri, Q2 FY26 concall, Nov 7, 2025

Through Q2 FY26, no new international wins. In Q3 FY26 (Feb 2026), the Ethiopia agri DPI was won (INR 25 Cr). 4 mandates across 3 markets. Verdict: Slower than the early talk suggested. Conversion materializing in a trickle.

Promise 6: PAN 2.0 will not impact Protean

“First of all, our mandate has not changed. We had a certain mandate from the department, the mandate has not changed... PAN 2.0 does not cover this mandate. It is a separate mandate completely.”

- Suresh Sethi, Q4 FY25 concall, May 22, 2025

This has been management’s consistent line across all four concalls. Through Q4 FY26, the PAN segment grew (FY26 Q4 PAN revenue grew YoY), and market share crept to 59%. The PAN 2.0 system has not yet gone live, so this is not yet truly tested. Verdict: Position reasonable so far. Final verdict in FY27 onwards.

Promise 7: Senior management stability

“It’s not a bulk sort of movement in that sense, but triggered for different reasons.”

- Suresh Sethi, Q3 FY26 concall, Feb 12, 2026

An analyst in the Q3 FY26 call called out senior management exits. Sethi attributed this to retirement and planned restructuring. Three months later (Q4 FY26 result), Sethi himself announced his departure on June 1, 2026. Verdict: Mark down on full transparency, but the exit itself is being handled smoothly.

Promise vs outcome summary

Overall management read

Management has been consistent with the numbers it calls out, honest about the segments where things are going slowly (Identity pricing, ONDC adoption), and willing to acknowledge what it doesn’t know (international conversion timing). The CEO transition introduces a key person dependency to test. Sandeep Mantri, in the CFO seat, provides accounting continuity. The 5-year track record shows a mixed picture on growth (revenue CAGR of about 4% from FY19 to FY25) but a clean balance sheet and no accounting controversies.

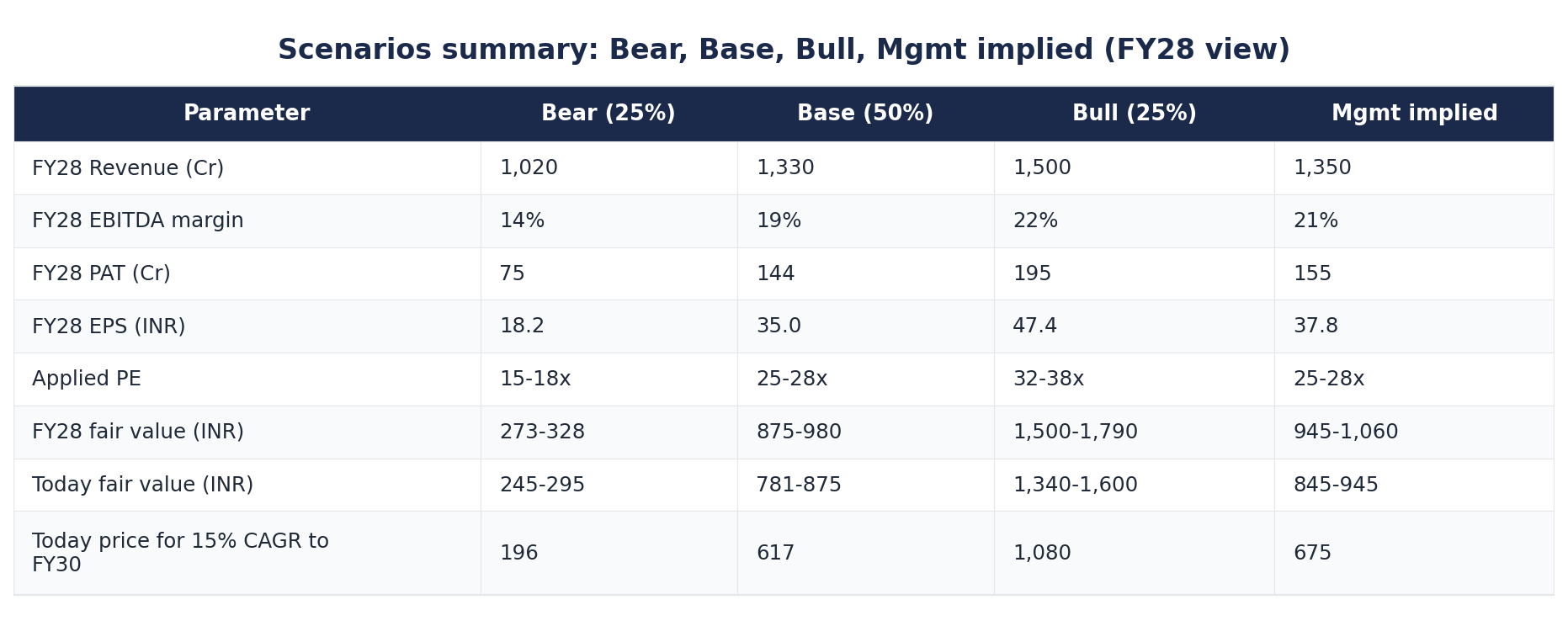

Section 10. Scenarios with valuation: bear, base, bull

Caveat. The numbers below are derived from management guidance, the FY26 reported financials, and the EPS-then-PE methodology requested. These are not recommendations. They are scenarios to think about, not advice to act on.

10.1 Starting point and approach

We start from FY26 reported numbers (consolidated):

Revenue from operations: INR 998 Cr

EBITDA: INR 188 Cr (18% margin)

Profit After Tax: INR 94.32 Cr

EPS (FY26): INR 22.93 (approx, on 4.11 Cr shares)

Cash and marketable securities: INR 850+ Cr

Order book: INR 1,600+ Cr (turnkey RFPs)

Current market price (May 21, 2026, post 20% upper circuit): approximately INR 648 on NSE

Market capitalisation: about INR 2,665 Cr

Trailing P/E (FY26 EPS): approximately 28x

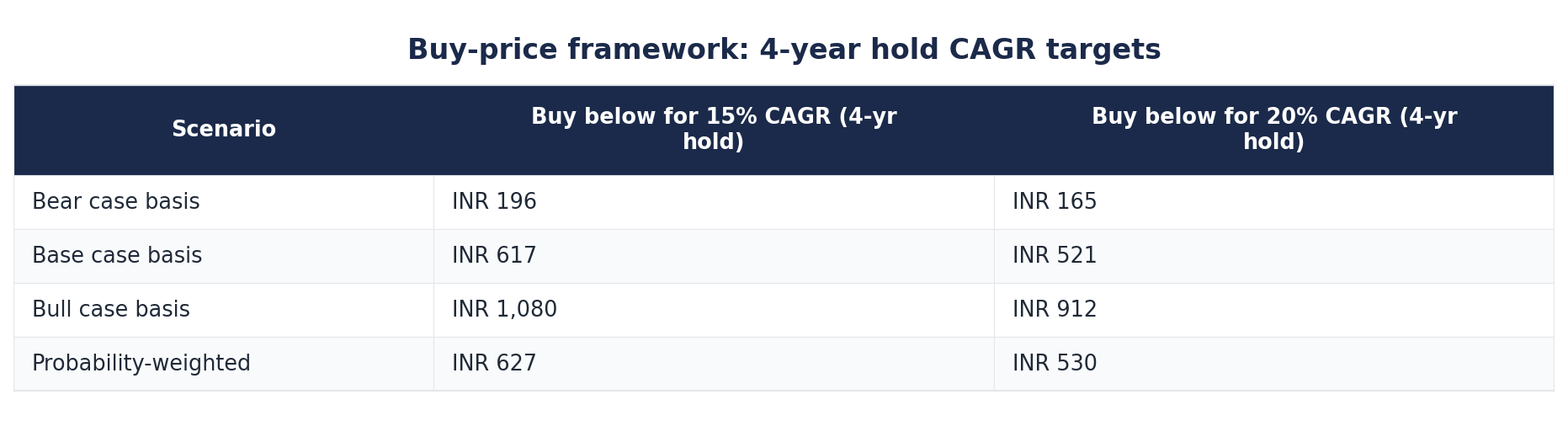

We project FY28 EPS in each scenario, assign a scenario-specific PE and derive a fair value range. We separately compute the price needed today to deliver a 15% CAGR over four years (to FY30) in each scenario.

10.2 BEAR case (probability: 25%)

The story. PAN 2.0 starts to crack the Tax Services franchise as the IT department gradually consolidates more of the workflow. Tax revenue declines 5% in FY27 and 8% in FY28. Identity margins compress further as Karza/Perfios and Signzy scale. CRA pricing transition takes longer than expected. ASK rollout slips, with full 190 centres only operational by Mar 2027 instead of Sep 2026. New Business contribution stalls at 16-17% of revenue. International wins remain sparse. New CEO struggles to articulate a clear direction in the first 3 quarters.

FY28 projections. Revenue INR 1,020 Cr (about flat). EBITDA margin compresses back to 14%. EBITDA INR 143 Cr. PAT INR 75 Cr. EPS INR 18.2. PE multiple deserves to compress to 15-18x in this scenario. Fair value at FY28: INR 273 to 328. Today’s fair value (1-year discount): INR 245 to 295.

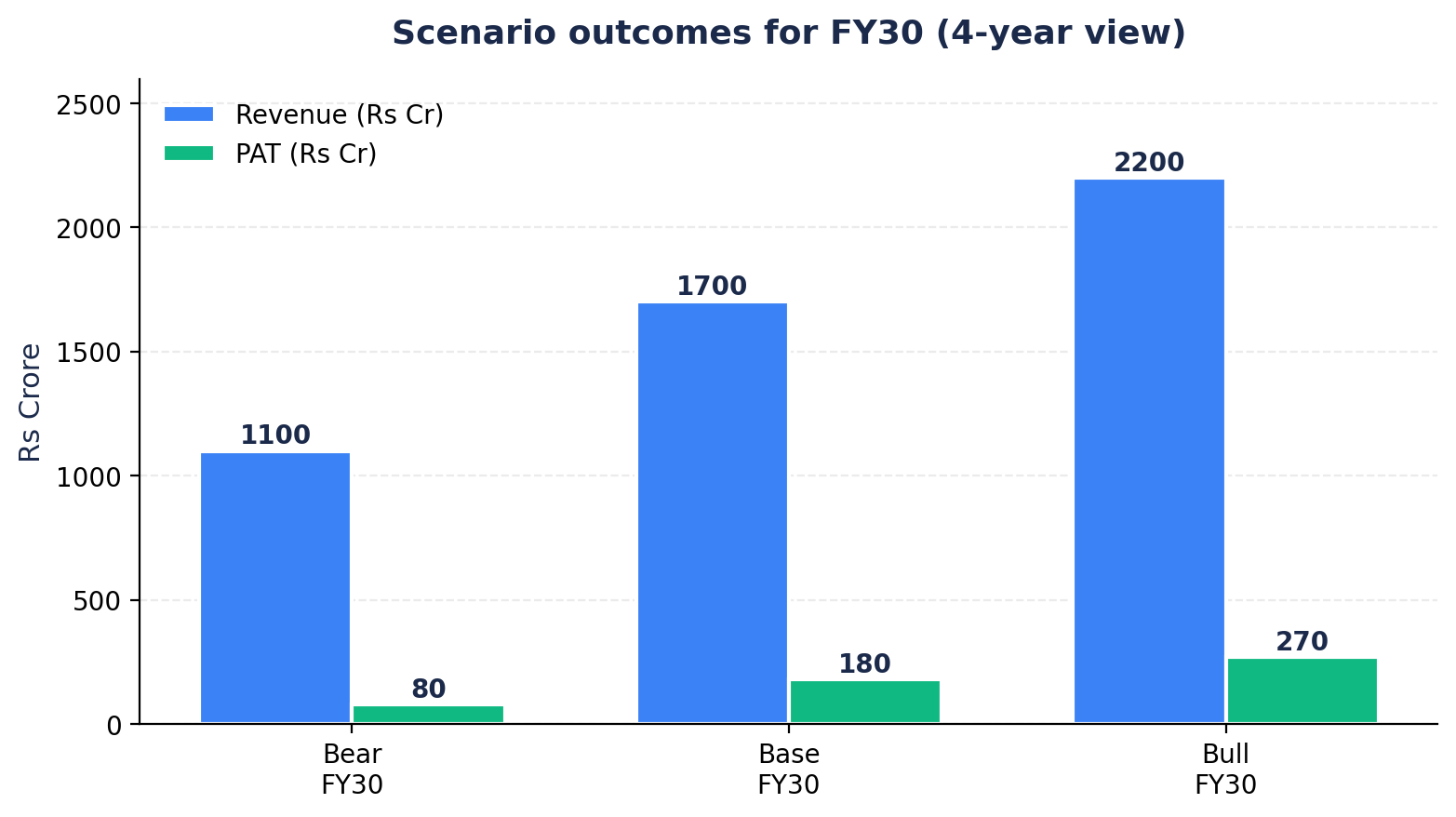

For 15% CAGR over 4 years to FY30: If FY30 PAT is INR 88 Cr and PE is 16x, FY30 fair price is INR 343. Today’s price for 15% CAGR: INR 196.

10.3 BASE case (probability: 50%)

The story. Management delivers on what it has publicly guided. ASK rolls out to 190 centres by end of FY27 (one quarter later than promised). INR 200 Cr ARR is visible by Q4 FY27 and full year by FY28. New Businesses cross 20% of revenue by FY28. CRA AUM-linked pricing tailwind kicks in by FY28 with subscriber base approaching 12 crore. Tax Services holds market share around 60% with modest volume growth. Identity stays low margin but stable. International contributes 3-4% of revenue. New CEO maintains strategic continuity.

FY28 projections. Revenue INR 1,330 Cr (15% CAGR FY26-FY28). EBITDA margin 19% (modest expansion). EBITDA INR 253 Cr. PAT INR 144 Cr (including some other income tailwind). EPS INR 35. PE multiple of 25-28x reasonable for a growing DPI specialist. Fair value at FY28: INR 875 to 980. Today’s fair value (1-year discount): INR 781 to 875.

For 15% CAGR over 4 years to FY30: If FY30 PAT is INR 185 Cr (continuing 14% growth), EPS INR 45, PE 24x, FY30 fair price is INR 1,080. Today’s price for 15% CAGR: INR 617.

10.4 BULL case (probability: 25%)

The story. Everything goes right. ASK rolls out on time and centres see higher than expected transaction volume. CERSAI and Bima Sugam deliver bigger annuities than guided. Multi-scheme framework drives a step-change in NPS subscriber adds; AUM-linked pricing structure compounds favourably. eSignPro and RISE become real INR 50 to 100 Cr SaaS lines by FY28. Two more international mandates land in FY27 (INR 50-80 Cr combined). Quantum-safe vault POC with RBI converts to commercial deployment. New Businesses exceed 25% of revenue in FY28. PE re-rates significantly as investor narrative shifts from “slow PAN issuer” to “DPI platform.”

FY28 projections. Revenue INR 1,500 Cr (22% CAGR FY26-FY28). EBITDA margin 22%. EBITDA INR 330 Cr. PAT INR 195 Cr. EPS INR 47. PE 32-38x as growth and quality both visible. Fair value at FY28: INR 1,500 to 1,790. Today’s fair value (1-year discount): INR 1,340 to 1,600.

For 15% CAGR over 4 years to FY30: If FY30 PAT is INR 260 Cr, EPS INR 63, PE 30x, FY30 fair price is INR 1,890. Today’s price for 15% CAGR: INR 1,080.

10.5 Management implied case

Management has guided: core businesses 8-12% growth, new businesses to be 25-30% of revenue in 3 years, EBITDA margin expansion of 300-400 bps. Applying those numbers to FY26 base gives FY28 revenue of about INR 1,290 to 1,380 Cr and EBITDA margin of 21%. PAT in management’s implied case is around INR 155 Cr, EPS roughly INR 38. With a 25-28x PE, fair value is INR 945 to 1,060. This is essentially the high end of our base case.

10.6 Analyst base case (sell-side)

Sell-side coverage is thin. Q4 FY26 estimates ranged INR 265-290 Cr revenue, INR 68-78 Cr PAT, EBITDA margin 34-36% (clearly aggressive). Q4 FY26 actual was INR 307.54 Cr revenue, INR 30.38 Cr PAT, EBITDA margin around 12-15%. Top-line beat; bottom line missed expectations. Analyst consensus broadly aligns with our base case.

10.7 Scenarios summary table

10.8 Buy-price thinking

What this means in plain English. If you assign 25% to the bear case, 50% to the base case, and 25% to the bull case, then today’s probability-weighted price below which you would expect a 15% CAGR over the next four years is about INR 627. The stock closed (or was trading intraday) around INR 648 on May 21, 2026, after a 20% upper circuit. So, at the current quote, an investor is paying a small premium to the probability-weighted 15% CAGR price. Whether that small premium is justified depends on whether you think the bull case is more likely than 25%.

10.9 The probability-of-profitability question

Protean is not a loss-making company. FY26 PAT is INR 94 Cr on operating EBITDA of INR 188 Cr. Operating earnings (excluding other income) at the contribution level were positive in every quarter of FY26 except Q3 FY25. Probability of remaining profitable through FY28: above 95%. The question for the stock is not whether Protean will be profitable, but whether profit will grow at a rate that re-rates the multiple back up from the current compressed levels.

10.10 Second and third order considerations

Cash optionality. INR 850 Cr cash is 32% of the market cap. Even if the operating business produces zero return, the cash earns 7-8% in short-dated instruments.

NSDL Payments Bank stake optionality. The 4.95% stake (INR 30.2 Cr invested) provides exposure to a regulated bank. If NSDL Payments Bank lists or attracts a strategic buyer, the holding could be revalued significantly.

Margin asymmetry of ASK. ASK is a transaction-fee model with minimum volume assured. Once the fixed cost of 190 centers is absorbed, every incremental transaction is high margin. Operating leverage in this segment is real and not fully priced in.

Quantum-safe vault sell-through. If RBI signs off on the white paper and Protean licenses the tech to other banks, that is an option not currently in any consensus number.

PAN 2.0 “all-clear” rerate. The stock is discounting a significant PAN 2.0 disruption. If the IT department’s distribution model remains unchanged through FY28, the implicit risk premium would compress.

CEO transition optionality. Ajay Rajan’s prior experience and any new strategic direction are a swing factor.

Negative second-order: if the new CEO embarks on a large acquisition with the cash pile, the option value of cash disappears overnight if the acquisition is mediocre.

Section 11. Annual report deep dive: green and red flags

11.1 Green flags

Zero debt balance sheet. Borrowings of INR 69 Cr at end of FY25 are entirely lease obligations under Ind AS 116 (right of use). No working capital debt, no term loans. Sustained through several years.

Robust cash conversion. Cash from operations INR 193 Cr in FY25 against PAT of INR 92 Cr (CFO/PAT of 2.1x). FY24 CFO was INR 58 Cr.

Debtor days improved from 81 (FY24) to 63 (FY25). Improvement driven partly by INR 36 Cr collection from ITD on long-pending storage charges.

Dividend payout discipline. 41-44% of PAT distributed as dividend in FY24, FY25 and FY26. INR 10 per share final dividend recommended for FY26.

Capex remained modest as % of revenue. Even with the ASK rollout, total capex stayed below 6-7% of revenue.

Auditor opinion unmodified for FY26. No qualifications. Statutory auditors signed off on May 20, 2026.

Order book at 1.6x revenue. INR 1,600+ Cr unexecuted order book vs FY26 revenue of INR 998 Cr provides forward visibility rarely seen in IT-enabled services.

Sovereign customer base reduces credit risk. Most counterparties are government or regulated entities. Bad debt risk is structurally low.

Pankaj Tripathi as brand ambassador. Spent on brand building to position the company beyond a B2B/B2G vendor.

Strong governance. Independent directors include experienced public sector and regulatory figures. Nandkumar Saravade joining as ID effective June 1, 2026.

11.2 Red flags and watch items

Operating margin compression FY22 to FY25. Reported OPM fell from 18% (FY22) to 10% (FY25). Recovered to 18% in FY26 but the multi-year erosion shows underlying business pressure.

Other income drives a meaningful share of EBITDA. FY25: PBT INR 118 Cr, of which INR 68 Cr was other income (treasury yield on INR 850 Cr cash). Operating profitability is thinner than headline EBITDA suggests.

5-year sales CAGR of just 3.26%. Revenue FY20 INR 716 Cr vs FY25 INR 841 Cr. The growth trajectory has not been linear. FY26 finally broke past FY24’s INR 882 Cr.

ECL (Expected Credit Loss) provisioning history. The INR 36 Cr ITD storage receivable was provisioned for many years before collection. While the eventual outcome was positive, this suggests the provisioning policy was conservative or the underlying delays were not fully transparent earlier.

Senior management exits in FY26. Several departures during the year. Followed by the announced exit of MD Suresh Sethi effective June 1, 2026.

Identity Services revenue decline despite volume growth. Volumes up across all four ID services but revenue down. Implies pricing pressure is structural, not temporary.

Q3 FY26 had a one-time INR 4 Cr labour code statutory impact. Adjusted PAT was INR 26 Cr; reported PAT was INR 22 Cr. The labour code transition is ongoing.

PAN 2.0 disclosure ambiguity. Management has spent every concall in FY26 reassuring on PAN 2.0. The level of management air-time devoted to this suggests the market sees the risk.

No clear segment-level profitability disclosure. Investors cannot directly assess whether Identity or New Businesses are running at a loss.

Stock has been a poor investment so far. Listed November 2023 at INR 792. Stock low touched INR 444 (March 30, 2026). Current quote post Q4 FY26 result around INR 648. IPO buyers are still well underwater.

11.3 Searching for number fudging or accounting concerns

We went through the publicly available FY24 and FY25 annual reports and quarterly disclosures looking specifically for issues:

No restatements of prior period figures.

Tax rate steady at 22-25%. No surprises, no abnormal deferred tax movements.

Other income breakup clear. Treasury income, interest and write-backs are disclosed separately. The INR 36 Cr storage charge collection was treated transparently.

Related party transactions are limited. NSDL group entities figured historically but post-demerger these have reduced.

Capitalised vs expensed boundaries seem reasonable. Intangible assets being amortised include the eSignPro, RISE and platform investments. Accelerated amortisation was taken in FY25 (which hurt reported earnings) rather than continued capitalisation.

No CBI, ED, SEBI or tax authority enforcement actions disclosed against the company or named directors as of May 2026.

No qualified audit opinion in any year we reviewed. FY26 declared with unmodified opinion.

Shareholding pattern shifts are transparent. Promoter holding 0% (post demerger from NSDL it is wholly public-held). FII holding rose to 8.62% post Q4 FY26.

Net read on annual report integrity. We did not find evidence of number fudging, accounting tricks, related-party concealment or regulatory enforcement actions. The business has visible operating challenges (margin compression, segment-level pressure) but they are disclosed and discussed. The auditor’s opinion is unmodified.

Section 12. Final verdict

This company has a perfect blend of tailwinds and headwinds: PAN 2.0 service, which accounts for 41% of revenue, could become obsolete in the future. On the other hand, e-identity, etc., is a commodity business and should not command a premium in valuation. The Aadhaar rollout, with 850 crore in cash, gives the company flexibility and optionality. The market does not like uncertainty. We have seen in the case of IEX that, quarter-on-quarter, it has shown good results, but the stock price has not moved; in fact, it has decreased. I will wait to see how PAN 2.0 will turn out. I strongly believe the era of agents is already over, and with AI adoption, we will see many startups that can solve your basic problems, like form filling.

As of now, this company is an avoid for me. I don’t think the market will re-rate any time soon, but nobody is supreme here; things can change quickly, and so can my and the market's perception of this stock.

Disclaimer: My hobby is studying business and posting here so I can come back and check how accurate my predictions were. I am not SEBI-registered, nor is this a buy-or-sell recommendation for this stock. Please do your due diligence before investing.

Please subscribe and share my blog